Part 6: What if legitimate competition emerges?

The impact of competition on ESRD patient experience, outcomes, and costs

A theme throughout this mini-series has been the role of competition (or lack thereof) in shaping the ESRD landscape into what it is today. One might assume if DaVita or Fresenius felt threatened, it could lead to more home dialysis (as incumbents offer a new modality to help differentiate) or a reduction in commercial reimbursement rates (as incumbents lose negotiating power).

Using 2019 dialysis facilities data from CMS, my goal is to test this assumption and project how legitimate competition might change the market[1].

What is legitimate competition?

I view competition as “legitimate” if it is positioned to acquire patients from existing dialysis providers. To do so, like incumbents, competitors could strategically form relationships with nephrologists (e.g., affiliation, employment) and convince those nephrologists to refer patients to their clinics. Competitors could also build such a superior product/experience that patients switch on their own. Two strategies that could potentially work:

Strategy 1: End-to-End Platform: Platforms treating CKD patients during Stages 1-4 develop relationships with those patients and nephrologists and thus are well-positioned to be the dialysis provider chosen if/when patients reach Stage 5. Strive and Somatus are trying this (though currently most focused on Stages 3 & 4). Also, akin to private equity’s typical healthcare play, a competitor could accomplish this by buying and integrating nephrologist practices with dialysis clinics in the same market.

Strategy 2: One Medical-ification: A “better” brick-and-mortar experience might be one where the clinics are nicer, run smoother, offer educational or social opportunities, or deliver additional clinical services to treat patients’ comorbidities (e.g., diabetes, pain from nerve damage).

If you recall, Part 2 described two types of patients: Type 1 patients (~35%) have a pre-existing relationship with a nephrologist prior to ESRD diagnosis whereas Type 2 patients (~65%) do not as they are diagnosed with ESRD following an emergency hospital stay. Admittedly, Strategy 1 is suited to acquire only Type 1 patients. Strategy 2 could theoretically acquire Type 2 patients but is more geared towards Type 1 as well. Type 2 patients are often referred to multiple clinics near their home immediately upon diagnosis, and the first clinic to respond and “accept” gets the patient. In my opinion, acquiring Type 2 patients at scale requires having both a vast footprint of clinics and fast response times, and I do not view that as a sustainable strategy.

The approach

Nevertheless, as discussed in Part 2, DaVita and Fresenius each hold 35%+ US market share, but since dialysis is delivered locally, competitive markets may still exist at the county-level. My goal is to understand the impact of competition by identifying those competitive markets and comparing them to non-competitive markets.

In the spirit of dialysis, I “filtered” for competitive markets as follows:

Lack of monopoly: Per the FTC, monopoly power does not exist if all firms have less than 50% market share within a geography[2]. Thus, any county where DaVita or Fresenius has 50%+ market share was excluded.

Options for patients: To ensure I included markets where patients could choose between different dialysis providers, any county without at least one facility from DaVita, Fresenius, and a non-DaVita or Fresenius provider was excluded.

Chart 1: Results of competitive market “filtering”[3]

Another look at the results:

Chart 2: Competitive vs. non-competitive market summary

Does competition breed a superior patient experience?

The leading indicator for dialysis clinic experience in the data1 was whether the clinic offered home hemodialysis (HHD) training and/or peritoneal dialysis (PD). As discussed in Part 4 & Part 5, HHD and PD create superior experiences for patients, but dialysis providers may lack the capabilities, agility, and/or incentives to deliver home dialysis at-scale.

Does the risk of losing patients in a competitive market motivate dialysis providers to differentiate by offering a more patient-centric dialysis modality? Nope. The percentage of facilities offering HHD training and/or PD is essentially the same regardless of competition.

Chart 3: Patient experience analysis

Some possible explanations:

Brick-and-mortar business model: In competitive markets, its presumably harder to fill the clinic, so perhaps providers question spending more money on HHD and PD when they are already struggling to recoup their clinic’s fixed costs.

Nephrologist constraint: Nephrologists are gatekeepers to patients, but many are not educated enough on home dialysis to refer patients to the modality. Nephrologist’s level of education in each market could impact dialysis providers decisions to offer home dialysis more than competition does (i.e., why offer if you’ll get no referrals?).

Game theory: The most mutually beneficial outcome for all dialysis providers might be to only offer in-center hemodialysis.

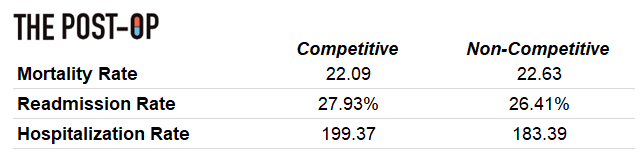

Does competition improve patient outcomes?[4]

Leading indicators for patient outcomes (at the facility-level) would be mortality rate (per 100 patient-years), readmission rate (as a percentage of hospital discharges), and hospitalization rate (per 100 patient-years). A quick explainer of patient-years: if 100 patients are followed for 2 years, that’s 200 patient-years. If 40 of those patients pass away, that would be a mortality rate of 40 deaths per 200 patient-years or 20 per 100 patient-years.

Chart 4: Patient outcomes analysis

As with experience, on average, there is limited difference in outcomes between competitive and non-competitive markets. Quick thoughts on possible explanations:

External factors such as income per capita, average age, etc. may be bigger drivers of outcomes and may not materially vary between competitive and non-competitive markets

Competition makes it harder to coordinate care (discussed further below)

Competition could dilute “talent” at the clinic-level; rather than the three best nurses at one clinic, they are spread across three clinics

Can competition reduce ESRD spend?

There is some interesting data available on ESRD Seamless Care Organizations (ESCOs) in CMMI’s Comprehensive ESRD Care (CEC) Model. Part 2 discusses it more, but as a refresh, dialysis providers, nephrologists, and others partnered to create ESCOs and participate in shared savings/losses payment models. The CEC Model started in 2015 and reportedly generated costs savings of $126 per beneficiary per month[5] compared to traditional ACOs. As of 2019 (i.e., Performance Year 4, most recent year with available data), there were 33 ESCOs covering 60,000 beneficiaries[6],[7].

So, if ESCOs generate savings, then if more ESCOs are set-up in competitive markets, maybe competition indirectly saves costs that way? The sample size is small, but based on 2019’s data, the answer is no.

Chart 5: ESCO analysis[8]

ESCOs require collaboration with nephrologists, so my hypothesis is most ESCOs were launched in non-competitive markets because, in these markets, dialysis providers were already engrained with the nephrologist network, making it easier to justify and set-up an ESCO. Further, in non-competitive markets, dialysis providers probably have relationships with a larger percentage of local nephrologists, making it easier to manage/coordinate care across their patient population.

Altogether, less competition might lead to better and/or more cost-efficient care. Greater competition creates more fragmentation, potentially making it harder to coordinate care (i.e., with more dialysis clinics battling to affiliate and/or integrate with nephrologists) and leading to higher costs.

More on competitive dynamics

If a competitor with Strategy 1 or 2 enters a local market with DaVita or Fresenius, how feasible would it be to acquire market share?

My assumption is that a competitor is unlikely to acquire patients already on dialysis as those patients will not change providers since they are accustomed to the routine, care team, etc. at their clinic. Perhaps a One Medical for dialysis could disprove this theory.

That leaves patients not yet receiving dialysis or new to dialysis as the most “acquire-able” for a competitor. Type 1 and a subset of Type 2 patients choose the clinic where they want to receive dialysis, and the biggest drivers of this decision are the clinics’ proximity to their home and/or whether their nephrologist (if they have one) rounds at/is affiliated with the clinic. So, even if a competitor has vastly superior quality and treatment modalities (and sometimes even proximity), it still needs nephrologists willing to refer patients to their clinic rather than DaVita and/or Fresenius’ (where the nephrologist likely has an existing affiliation).

For context, DaVita claims 5,400+ nephrologists are currently referring to their dialysis centers, and given DaVita is in 700+ markets, that means they have relationships with 7-8 nephrologists per market[9]. This dynamic greatly increases barrier to entry and explains why I believe legitimate dialysis competitors need to be ‘end-to-end’ and be closely linked to/even own the nephrologist-patient relationship throughout the patient’s journey.

Parting shot

In close, I think there is a pessimist vs. optimist debate here. Pessimists say competition won’t fix the problems since the data implies competition doesn’t impact experience, outcomes, or cost. Optimists would say maybe DaVita and Fresenius just don’t feel threatened enough by the current landscape of dialysis providers. Optimists might also say incumbents’ businesses remain incredibly sensitive to commercial patient attrition (as discussed in Part 3), so while barriers to entry are high, it won’t take much to make them feel threatened.

***

Links to: Sources | Analysis (Excel) | Graphics (PPT)

This was probably my favorite part of the series to write, so if you’d like to discuss further, feel free to connect with me on Twitter @z_miller4 or on LinkedIn here!

Beat the Bruins!!!